Hey,

Most product teams think hypergrowth proves they are right. That belief is incomplete. Sometimes it is flat out wrong.

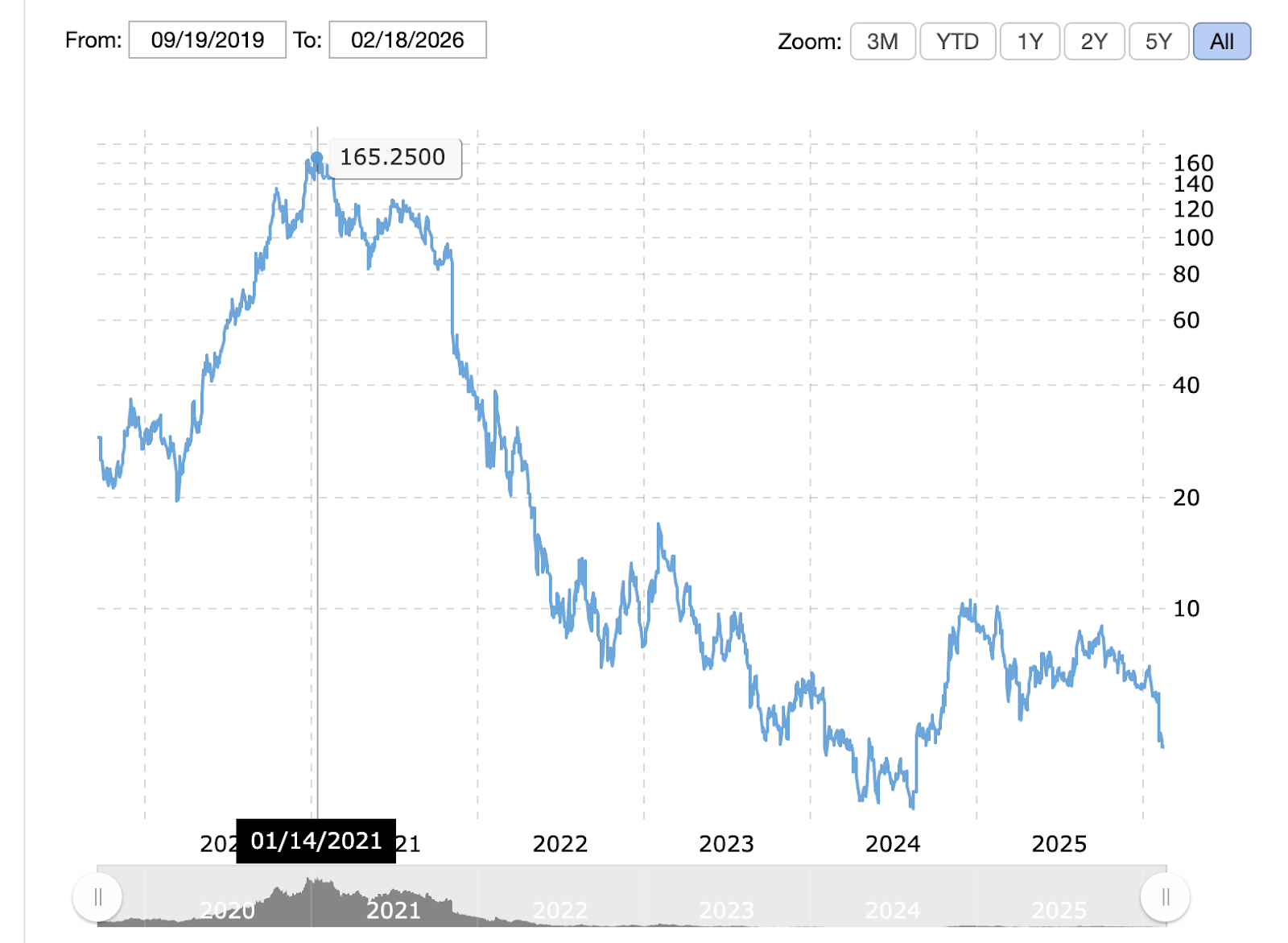

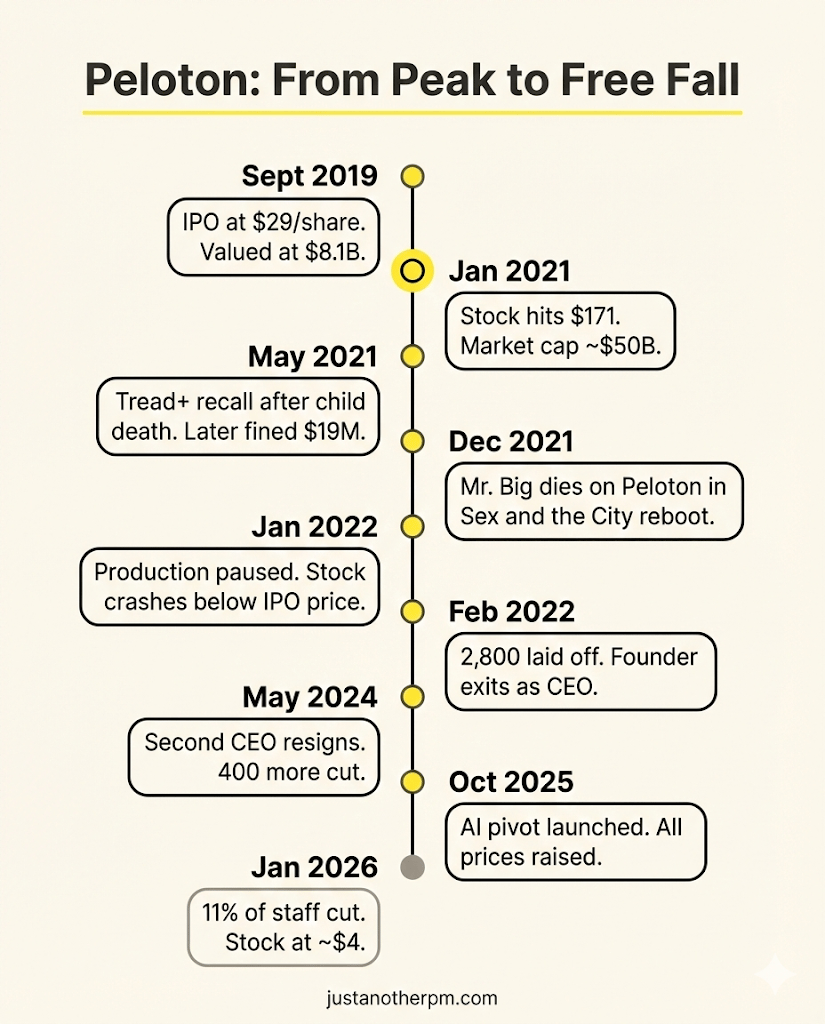

The best example is Peloton. If you had invested $1,000 in Peloton at its IPO in September 2019, it would be worth roughly $37 today. Thirty-seven dollars. Not $37,000. Not $3,700. Thirty-seven dollars.

That is a 97% collapse in shareholder value. But this was a company that:

- Made its founder a billionaire

- Turned instructors into celebrities

- Convinced Wall Street that the future of fitness lived in your bedroom

- Reached nearly $50B in market capitalization

Two weeks ago, on January 30, 2026, Peloton cut 11% of its remaining workforce. It was the fourth major layoff in less than four years. Most of the cuts hit engineers, the same teams building the AI features Peloton launched just three months earlier as its comeback strategy.

So how does a company go from $50B to roughly $1.8B in five years?

The answer isn't just "the pandemic ended." It's a story about a product team that mistook a temporary behaviour shift for a permanent one, scaled for a future that never arrived, and then kept making the wrong bets trying to find its way back.

What happened was predictable. And if you are building AI products in a high-growth cycle right now, this case should make you uncomfortable.

Let’s break it down.

A Kickstarter Bike and a Crazy Idea

In 2011, John Foley was a Barnes & Noble executive in New York with two young kids and not enough time to get to the gym. He loved boutique cycling classes — the energy, the music, the instructor pushing you harder than you'd push yourself. But fitting a 45-minute class into a packed schedule was nearly impossible.

His insight was simple: what if you could stream a world-class cycling class directly into someone's living room?

Foley pitched the idea to his colleague Tom Cortese over dinner. Together with three more co-founders — Graham Stanton, Hisao Kushi, and Yony Feng — they built a test bike using off-the-shelf hardware and an Android tablet bolted to the handlebars.

They launched a Kickstarter in summer 2013. The goal was $250,000. They raised $307,000 — enough to prove there was interest, but at $1,500 per bike, they'd pre-sold fewer than 200 units. The idea of a $2,000 stationary bike with a screen seemed absurd. Who would pay that when gym memberships averaged $58 a month?

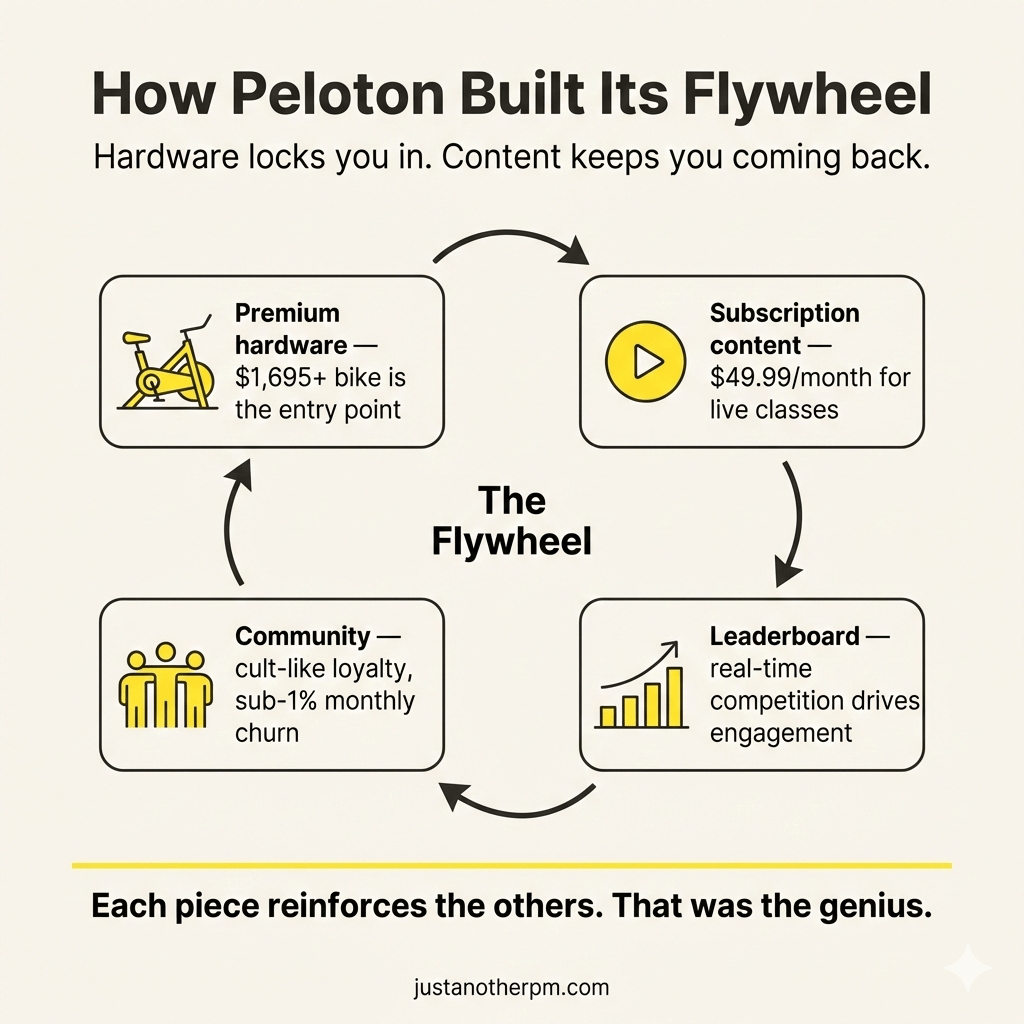

But there was a detail most people missed. Peloton wasn't really a hardware company. It was a media company that happened to sell bikes.

The bike was just the delivery mechanism.

Here is what they actually built:

1. Hardware as the entry point: The bike created an experience in the home.

2. Subscription as the revenue engine: $39 per month for unlimited live and on-demand classes.

3. Content as the retention driver: Instructors became personalities. Classes felt lively and communal.

4. Leaderboard as the engagement loop: Real-time output tracking created competition and accountability.

Now, that was a closed ecosystem. Peloton controlled hardware, software, content production, and distribution. Every layer strengthened the next.

The sensors tracked performance. Performance fed the leaderboard. The leaderboard drove competition. Competition drove engagement. Engagement reduced churn. That loop was intentional.

By 2016, the company made $60 million in annual revenue. By 2018, revenue was roughly doubling year over year.

That growth was the result of deliberate product architecture.

If you are building AI products today, pay attention to this part. Vertical integration increases control and defensibility.

But it also increases capital intensity and operational risk. Early on, that integration was Peloton’s strength. Later, it would magnify the downside.

The IPO Validation and Risk

On September 26, 2019, Peloton went public on the Nasdaq at $29 per share, raising $1.16 billion and valuing the company at $8.1 billion. It had over 500,000 connected fitness subscribers. Revenue for the fiscal year had hit $915 million — more than doubling from the year before.

The stock actually dipped below its IPO price on the first day. Investors had concerns. The bikes were expensive. The company was losing money — $195.6 million in net losses that fiscal year.

And there was an awkward PR moment: a holiday ad in November 2019 showed a husband gifting his wife a Peloton bike, which the internet promptly roasted as tone-deaf.

The actress from the ad was quickly hired by Aviation Gin to star in a parody commercial mocking the original.

But something more important was happening beneath the surface. Peloton's customers were fanatically loyal. The monthly churn rate was under 1%. People were getting Peloton logo tattoos. Hugh Jackman, Usain Bolt, and Richard Branson were members. The community had a cult-like devotion that most consumer brands can only dream about.

This is the kind of product-market fit that makes investors salivate. Low churn. High engagement. A subscription model with predictable recurring revenue. And a customer acquisition cost of just $5 per connected fitness subscriber.

Then the world changed.

The Pandemic Rocket Ship

In March 2020, gyms across the world shut down. Overnight, the question shifted from "who would pay $2,000 for a stationary bike?" to "where do I sign up?"

Peloton's stock, which had been hovering around $23 during the market panic, began a historic rally. By the end of 2020, it had risen over 440%. On January 14, 2021, it hit an all-time intraday high of $171.09 — giving Peloton a market capitalisation of nearly $50 billion.

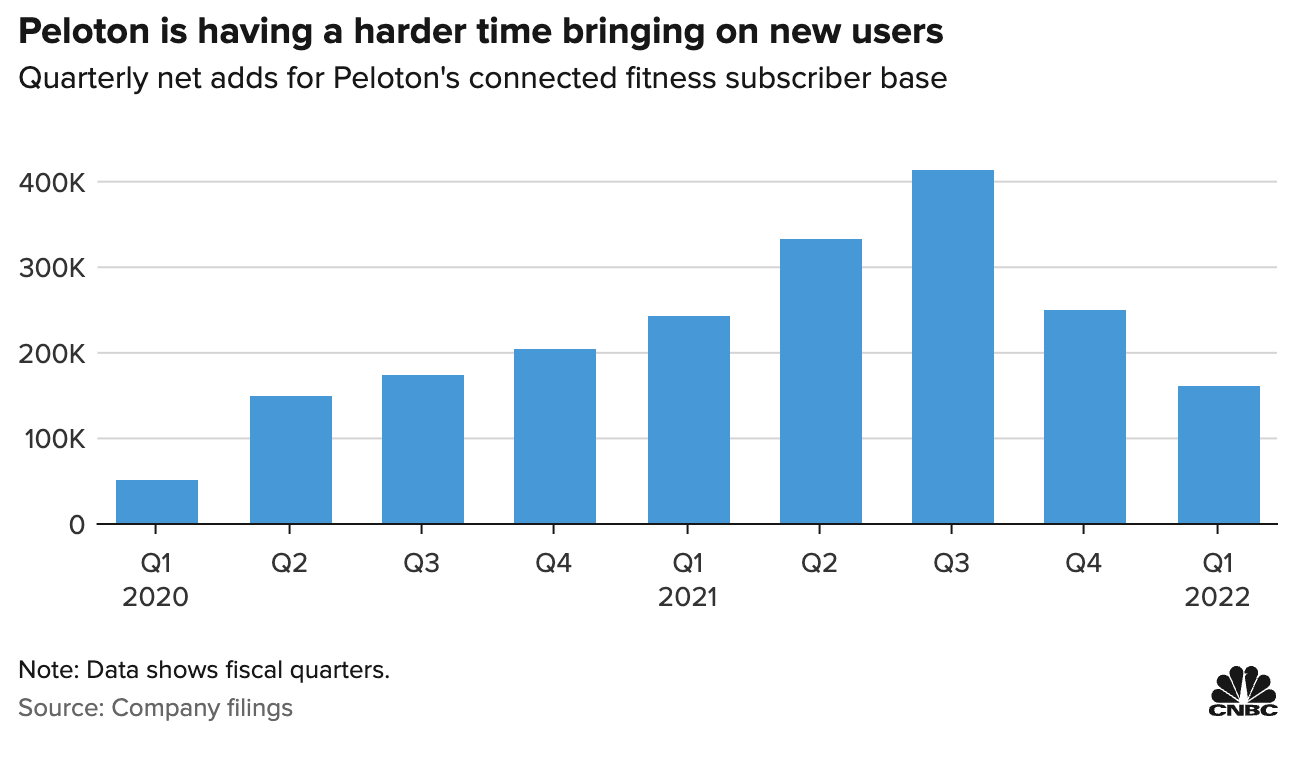

The numbers were staggering. Revenue surged from $915 million in fiscal 2019 to over $4 billion by fiscal 2021. The subscriber base exploded. Monthly workouts per subscription rose from about 8 in 2018 to 22 in 2021. For three consecutive quarters, Peloton actually turned a profit.

This is where the story gets interesting — and where the product decisions start to go wrong.

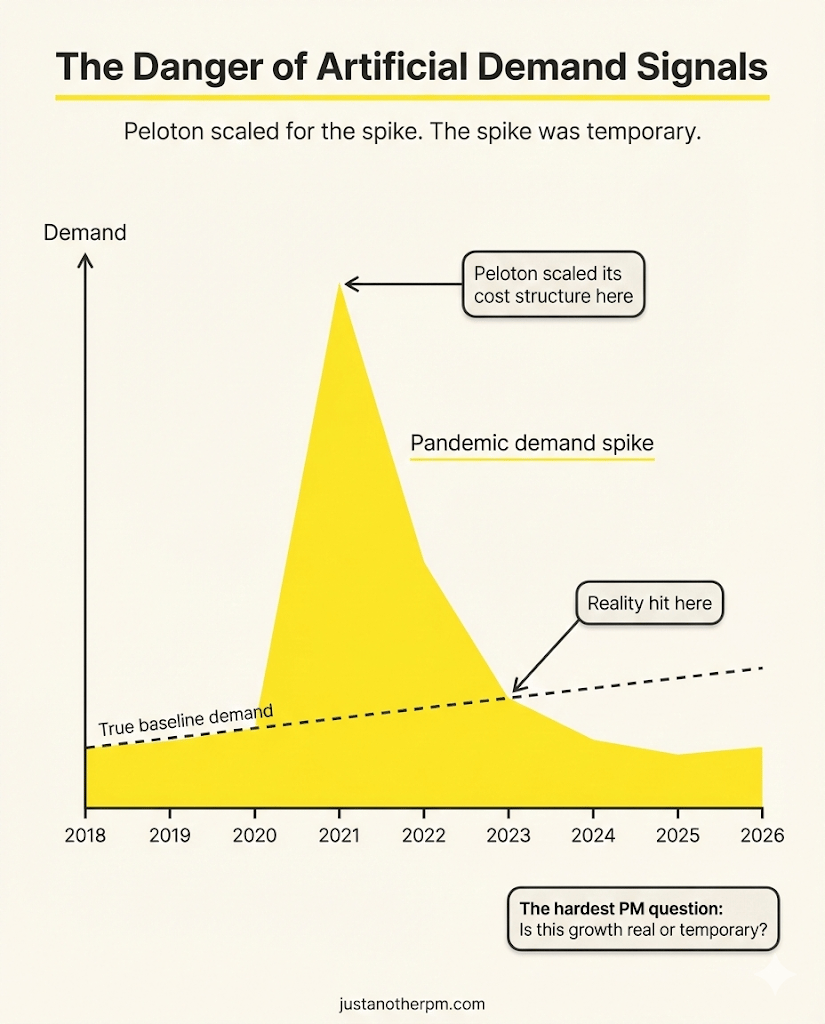

Peloton looked at the pandemic demand and made a fateful assumption: this is the new normal.

The company went on a massive spending spree. It acquired Precor, a commercial fitness equipment maker, for $420 million. It hired aggressively. It expanded its product line, launching the Tread treadmill and planning more hardware.

From a product strategy perspective, this was the critical error. Peloton was scaling its cost structure for sustained hypergrowth — at the exact moment the growth was about to reverse.

The difference between pandemic demand and real demand is one of the hardest things for any product team to assess in the moment. When your metrics are all pointing up and to the right, questioning whether the trend is sustainable feels like pessimism. But the best product leaders build for the most likely future, not the most exciting one. Peloton built for the exciting one.

Everything Broke at Once

The decline happened in waves.

Spring 2021 marked the turning point. From that point forward, three separate failures compounded each other: safety, perception, and demand.

1. The Treadmill Crisis

In May 2021, the U.S. Consumer Product Safety Commission urged the brand to recall its Tread+ treadmill after a six-year-old child died in an accident involving the machine.

There were more than 150 incidents reported involving people, pets, and objects being pulled under the rear of the treadmill.

The issue was serious. And how the brand responded made it worse. Peloton initially told the regulator’s warnings were inaccurate and misleading and refused to recall the product.

The consequences were at the same level. It paid a $19 million civil penalty for poor reporting and for continuing to distribute recalled treadmills. Soon, what started as a safety issue became a trust issue.

A premium brand built around wellness and community chose to challenge regulators before protecting customers. That damaged credibility at the exact moment the company needed investor confidence.

The lesson is that when safety is involved, transparency and speed are not optional. Fighting the regulator rarely protects long-term value.

2. Cultural Perception Collapsed

In December 2021, the Sex and the City reboot And Just Like That... aired an episode where the beloved character Mr. Big dies of a heart attack after riding a Peloton bike. A few weeks later, a character on Billions suffered a similar fate on a Peloton. The stock dropped further each time. It was absurd, but it mattered — because by this point, investor confidence was already fragile.

3. The Demand Cliff

As vaccines rolled out and gyms reopened, Peloton's growth engine stalled. New subscriber additions slowed dramatically. The company had massively overbuilt inventory. In January 2022, CNBC reported that Peloton had temporarily paused production of its bikes and treadmills because demand had evaporated, leaving a glut of unsold hardware.

The stock, which had already fallen 76% during 2021, crashed through its IPO price of $29.

Liking this post? Get the next one in your inbox!

Three CEOs in Four Years

His replacement was Barry McCarthy, the former CFO of both Netflix and Spotify — two companies that had successfully built massive subscription businesses. The logic was clear: Peloton needed someone who understood how to run a subscription-first company, not a hardware-first one.

McCarthy tried to shift the model. He opened up distribution through Amazon and Dick's Sporting Goods. He introduced rental programmes. He cut costs. But the fundamental problem remained: Peloton's subscriber base had stopped growing, and the hardware that was supposed to be the entry point to the ecosystem was gathering dust in warehouses.

By May 2024, McCarthy resigned after just two years. Peloton announced another 15% staff reduction — roughly 400 more employees — and brought in Peter Stern, a former Apple and Ford executive, as the new CEO starting January 2025.

Three CEOs in four years. Each one inheriting a more diminished version of the company the previous one received.

The AI Hail Mary

By late 2025, the growth problem was clear. Subscriber numbers were shrinking. Hardware demand was weak. Revenue was declining.

So Peloton made its biggest strategic bet in years.

In October 2025, CEO Peter Stern revealed what the company described as “the biggest reinvention in its history.” They refreshed the entire hardware lineup under a new “Cross Training Series” brand.

The screens on every machine now rotate 360 degrees, turning the bike into a platform for yoga, strength training, and pilates. The plus models come with movement-tracking cameras and speakers co-developed with Sonos. It was ambitious. It was polished. And it came with a significant catch.

The Bike went from $1,445 to $1,695. The Bike+ jumped to $2,695. The Tread+ hit $6,695 — a $700 increase. And the monthly subscription rose from $44 to $49.99, the first price increase in three years.

Peloton was betting that AI features would justify premium pricing and bring lapsed customers back. The early results suggest otherwise. In its most recent earnings report on February 5, 2026, revenue came in at $657 million — below both Wall Street expectations and Peloton's own guidance. Connected fitness subscribers fell to 2.661 million, down 7% year-over-year. The stock dropped roughly 26% in a single day.

CEO Stern acknowledged on the earnings call that the company had overestimated how many existing members would upgrade to new hardware. The equipment was durable enough that people simply didn't feel the need to replace it. Which is an ironic problem for a premium product company: you built it too well for people to want a new one.

Where It Stands Today

As of mid-February 2026, Peloton's stock trades around $4.25. Its market capitalisation is roughly $1.8 billion. To put that in perspective: at its peak in January 2021, Peloton was worth nearly 28 times what it's worth today.

The company still has 2.66 million paying connected fitness subscribers, which is nothing to dismiss. Churn remains low. Margins are actually improving — gross margin hit 50.5% last quarter. And subscription revenue, at $413 million for the quarter, still forms a solid base.

But revenue keeps declining. The subscriber base keeps shrinking. And the three rounds of layoffs in the past 18 months — 6% in August 2025, 11% in January 2026 — have hollowed out the engineering teams that were supposed to build Peloton's AI-powered future.

The company is now on its third CEO. Its CFO announced her departure on the most recent earnings call. It faces a $65 million hit from tariffs. And it's trying to grow by expanding into commercial fitness (hotels, gyms, corporate wellness) while simultaneously cutting the people who would build that expansion.

In a Nutshell

The tempting narrative is that Peloton was just a pandemic fad. That's partly true but mostly lazy.

Peloton built something genuinely innovative before the pandemic. The vertical integration of hardware, software, and content created one of the stickiest consumer products of the 2010s. The community and instructor model was legitimately differentiated. The subscription metrics were best-in-class.

The deeper lesson is about how product teams respond to artificial demand signals. When COVID hit, Peloton's metrics went vertical. Everything said "scale." But the right move — the one that's nearly impossible to make when the board is euphoric and the stock is soaring — was to ask: how much of this demand will survive the return to normal?

Instead, Peloton spent like the boom was permanent.

Then there's the question every product team should wrestle with: what happens when your core value proposition is tied to a constraint that disappears? Peloton's magic was bringing the gym experience home. When gyms reopened and people could choose where to exercise again, "the gym at home" became "an expensive coat rack in the bedroom" for millions of users.

The AI pivot tells its own story. Peloton IQ is a perfectly reasonable feature set. But bolting AI onto a product whose core problem is demand — not features — is a pattern we see across struggling tech companies right now. When sales are declining, adding complexity and raising prices is a risky bet. Especially when your most loyal users chose you for simplicity: get on the bike, clip in, follow the instructor, feel great.

The question for Peloton has never been whether the product is good. It's always been good. The question is whether there are enough people willing to pay a premium for an at-home fitness subscription when the world offers infinite alternatives — from a $10 Planet Fitness membership to a free YouTube workout to simply going for a run.

That question still doesn't have a clear answer. And that's what makes Peloton's story so instructive. Not every great product builds a great business. Sometimes the market you're building for is smaller than you think. And the hardest skill in product management isn't building — it's knowing when to stop.

What do you think — is Peloton's AI bet the start of a real comeback, or just another chapter in the decline? Reply and let me know.

More from

Other